To OurShareholders, Employees and Guests

Chairman and

Chief Executive Officer

President and

Chief Operating Officer

Our financial performance in fiscal 2013 was certainly disappointing, with sales and earnings results that were well below what we expected when the year began. As we emerge from the year, however, we have greater clarity about what we have to do to regain operating momentum in fiscal 2014 and remain the leader in our industry long term. We have to achieve consistent guest traffic growth in existing restaurants. And to do that, we have to deliver guest experiences that are more responsive to several important consumer and competitive realities.

Fiscal 2013 Financial Highlights

We will review our fiscal 2013 financial performance, then discuss the strengths we bring to the challenge of reigniting traffic growth, the consumer and industry dynamics driving the need for change and our response to those dynamics.

| Fiscal Year Ended (In Millions, Except Per Share Amounts) |

May 26, 2013 | May 27, 2012 | May 29, 2011 | |

| Sales | $ 8,551.9 |

$ 7,998.7 |

$ 7,500.2 |

|

| Earnings from Continuing Operations | $ 412.6 |

$ 476.5 |

$ 478.7 |

|

| Losses from Discontinued Operations, net of tax | $ (0.7) |

$ (1.0) |

$ (2.4) |

|

| Net Earnings | $ 411.9 |

$ 475.5 |

$ 476.3 |

|

| Earnings per Share from Continuing Operations: | ||||

Basic |

$ 3.20 |

$ 3.66 |

$ 3.50 |

|

Diluted |

$ 3.14 |

$ 3.58 |

$ 3.41 |

|

| Net Earnings per Share: | ||||

Basic |

$ 3.19 |

$ 3.65 |

$ 3.48 |

|

Diluted |

$ 3.13 |

$ 3.57 |

$ 3.39 |

|

| Dividends Paid per Share | $ 2.00 |

$ 1.72 |

$ 1.28 |

|

| Average Shares Outstanding: | ||||

Basic |

129.0 | 130.1 | 136.8 | |

Diluted |

131.6 | 133.2 | 140.3 | |

|

||||

Despite blended same-restaurant sales and traffic declines at our three large brands (Olive Garden, Red Lobster and LongHorn Steakhouse), we had significant total sales growth in fiscal 2013, due to growth in sales from new restaurants, same-restaurant sales growth at our Specialty Restaurant Group (SRG) and our acquisition of Yard House USA, Inc. on August 29, 2012. However, some of the steps we took to mitigate same-restaurant sales and traffic erosion at Olive Garden and Red Lobster and support continued same-restaurant sales and traffic growth at LongHorn Steakhouse adversely affected margins. In addition, we incurred costs in connection with our acquisition of Yard House. Because of these and other factors, our diluted net earnings per share from continuing operations declined in fiscal 2013.

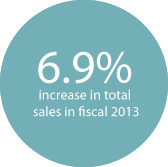

- Total sales from continuing operations were $8.6 billion, a 6.9 percent increase from the $8.0 billion generated in fiscal 2012. Excluding sales from Yard House, total sales from continuing operations were $8.3 billion, a 3.7 percent increase from fiscal 2012.

- Total sales growth from continuing operations in fiscal 2013 reflected a combined U.S. same-restaurant sales decrease of 1.3 percent for Olive Garden, Red Lobster and LongHorn Steakhouse; a combined U.S. same-restaurant sales increase of 2.1 percent for our Specialty Restaurant Group, including The Capital Grille®, Bahama Breeze® and Seasons 52®, but excluding Eddie V’s and Yard House; 3.6 percent of growth compared to fiscal 2012, due to the acquisition of 40 Yard House restaurants and four additional Yard House openings; and 4.4 percent of growth due to the net addition of 100 other new restaurants.

- Net earnings from continuing operations were $412.6 million in fiscal 2013, a 13.4 percent decrease from net earnings from continuing operations of $476.5 million in fiscal 2012. Diluted net earnings per share from continuing operations were $3.14 in fiscal 2013, a 12.3 percent decrease from diluted net earnings per share of $3.58 in fiscal 2012. In fiscal 2013, costs associated with the Yard House acquisition reduced net earnings from continuing operations by $12.3 million (on an after-tax basis) and diluted net earnings per share by $0.09.

- Olive Garden’s total sales were $3.68 billion, up 2.9 percent from fiscal 2012. This reflected average annual sales per restaurant of $4.6 million, the addition of 36 net new restaurants and a U.S. same-restaurant sales decrease of 1.5 percent.

- Red Lobster’s total sales were $2.62 billion, a 1.7 percent decrease from fiscal 2012. This reflected average annual sales per restaurant of $3.7 million, the addition of one net new restaurant and a U.S. same-restaurant sales decrease of 2.2 percent.

- LongHorn Steakhouse’s total sales were $1.23 billion, up 10.3 percent from fiscal 2012. This reflected average annual sales per restaurant of $3.0 million, the addition of 44 net new restaurants and a U.S. same-restaurant sales increase of 1.2 percent.

- The Specialty Restaurant Group’s total sales were $986 million, a 58.3 percent increase from fiscal 2012, and reflected strong growth from our legacy brands as well as the addition of Yard House. Total sales increased 8.5 percent at The Capital Grille to $332 million, based on same-restaurant sales growth of 3.3 percent and the addition of three new restaurants. Total sales increased 12.6 percent for Bahama Breeze to $174 million, based on same-restaurant sales growth of 0.2 percent and the addition of three new restaurants. Total sales increased 23.3 percent at Seasons 52 to $158 million, based on same-restaurant sales growth of 1.2 percent and the addition of eight new restaurants. Total sales increased 84.4 percent at Eddie V’s to $65 million, based on same-restaurant growth of 0.7 percent, the addition of one new restaurant and approximately five months of incremental sales compared to fiscal 2012 because our acquisition of Eddie V’s occurred in November of fiscal 2012. In addition, the acquisition of 40 Yard House restaurants and opening of another four Yard House restaurants following the acquisition added $258 million in sales in fiscal 2013.

- We continued to buy back Darden common stock, spending $52 million in fiscal 2013 to repurchase 1 million shares, before postponing share repurchase in August 2012 because of the acquisition of Yard House. Since our share repurchase program began in 1995, we have repurchased nearly 172 million shares of our common stock for $3.82 billion.

A Strong Foundation

As we look forward, we approach the challenges ahead with a very strong foundation. The most important foundational strength is our brands, starting with the three largest. Each has enduring and broad consumer appeal, which shows in their number of restaurants, average annual sales per restaurant and restaurant-level returns. With respect to average sales per restaurant, Olive Garden and Red Lobster have long been leaders on this important measure, compared to other nationally advertised casual dining chains. That continues to be true, despite a difficult fiscal 2013. At LongHorn Steakhouse, average sales per restaurant are solid as well, especially considering that the amount the brand spends on television advertising is a fraction of the amount spent by most nationally advertised chains, including Olive Garden and Red Lobster. In addition, within our Specialty Restaurant Group, each brand’s average sales per restaurant is among the highest in the restaurant industry, regardless of industry segment. Importantly, all our brands are able to translate competitively strong average sales per restaurant into competitively superior restaurant-level returns.

In addition to strong brands, we have a cost-effective operating support platform. It is the product of considerable collective expertise and experience in areas that are critical to success in our business, including brand management, restaurant operations, supply chain, talent management and information technology. With appealing brands that have strong restaurant-level returns and are supported by a cost-effective operating platform, we have a competitively superior operating profit margin compared to other major chain restaurant operators with comparable, primarily company-owned business models. The net result is that we have substantial and durable operating cash flow. Our operating cash flow has nearly doubled over the past 10 years, growing to $950 million in fiscal 2013 — or $515,000 in pre-tax cash per restaurant — despite our setbacks during the year. Together, these strengths provide us with a strong foundation as we respond to the important consumer and competitive realities that, we believe, amount to a New Era.

Operating in a New Era

Key Consumer And Competitive Dynamics

The consumer and competitive dynamics driving the need for change have been a reality for several years. One important dynamic is that many guests are financially constrained. For some, this is a matter of life stage. These are guests who are more budget conscious because they are young and just entering the workplace or, at the other end of the spectrum, because they have recently retired and are beginning to live on fixed incomes. For other guests, financial constraint is due to macroeconomic factors having nothing to do with life stage that are weighing on employment and income growth. Whatever the reason, the result is a significant number of guests who increasingly base their restaurant choices on affordability.

At the same time, many other guests are far from financially constrained. They have changing tastes and preferences that reflect rising household incomes and are increasingly interested in higher-quality, on-trend menu offerings and flexible experiences that fit their schedules. In addition, both sets of guests — the financially constrained and the financially comfortable — are increasingly multicultural and multigenerational, developments that are also driving meaningful changes in tastes and preferences.

Given these dynamics, as we entered fiscal 2013 there had been an approximate 2 percent a year decline in total casual dining traffic between fiscal 2008, when the most recent recession started, and fiscal 2012. Importantly, major casual dining chains had held up better than casual dining overall, with cumulative total traffic growth of 0.6 percent over this period, fueled in part by a sharp increase in price incentives. In addition, during this period Darden achieved a significant gain in market share, with our three large brands experiencing cumulative total traffic growth of 10.1 percent.

However, below the total traffic growth level, a concerning development for major chains and for us was the steady erosion in same-restaurant traffic over this period. Between fiscal 2008 and fiscal 2012, major chains had an 18.2 percent decline in same-restaurant traffic on a cumulative basis. And, while our three large brands did better, on a blended basis our same-restaurant traffic declined 7.7 percent on a cumulative basis.

Responding To The Dynamics

As fiscal 2013 began, we had already made a number of changes to address the consumer realities behind the same-restaurant traffic erosion the casual dining industry and we were experiencing, and we were planning additional steps. To broaden our guest base, especially with more affluent guests and Millenial and Gen X guests, we had been adding to our Specialty Restaurant Group — first with the acquisition of Eddie V’s in fiscal 2012 and, more significantly, with the acquisition of Yard House, which was in the due diligence stage early in fiscal 2013 and completed at the very beginning of the second quarter. In addition, each of our three large casual dining brands had affordability initiatives planned for fiscal 2013, with a focus on both our promotional offers and core menus.

At the Darden level, we had launched several initiatives to address consumer interests beyond affordability that continued during fiscal 2013. In fiscal 2012, for example, we developed a multiyear plan to enhance our technology capabilities so we will be able to engage as fully as possible with guests as they lead increasingly digital lifestyles, and we planned to begin implementing the first phase in fiscal 2013. We had also established an enterprise Marketing group to focus on developing more extensive, multiyear initiatives to reshape the guest experiences we offer, and planned to begin implementing several of these in fiscal 2013 as well. We also recognized the need to reshape our Marketing and Operations teams at each brand so that we could be brilliant with the basics today, while also moving faster to make enduring changes to the guest experiences we offer in the future. As a result, coming into fiscal 2013 we were rethinking how we should organize our large brands’ Marketing and Operations teams.

Accelerating Change In Fiscal 2013

As fiscal 2013 unfolded, it quickly became clear that the degree and pace of change we had planned for the year was insufficient. In the fourth quarter of fiscal 2012, for the first quarter since the start of the recent recession in fiscal 2008, blended same-restaurant traffic at our three large brands lagged the industry. As we continued to have weaker than the industry results on this important profitable sales growth driver in the first two quarters of fiscal 2013, we moved with added urgency on a number of fronts.

We began to match competitive promotional intensity around affordability, which involved being more aggressive with the pricing of our offers, placing greater emphasis on price in our advertising messages and being more active in the use of tactics such as daily and weekly digital specials to support our offers.

We also stepped up the emphasis on affordability in our core menus, which included launching with heavy media support of a new core menu at Red Lobster that has a significant affordability component and accelerating the introduction of new, more affordably priced core menu offerings at Olive Garden and LongHorn Steakhouse.

Just as importantly, we increased the resources dedicated to reshaping our guest experiences to respond to what guests want beyond affordability. Among other things, this included moving forward more quickly with the reorganization of the Marketing and Operations teams at our three large brands and ramping up investment in enhancing our digital and targeted marketing capabilities.

Our same-restaurant traffic results in the third and fourth quarters of fiscal 2013 are evidence that these steps provided us with some traction. In the third quarter, our results matched the results for the industry, although it was not a strong quarter, given the magnitude of the traffic decline for us and for the industry. In the fourth quarter, however, we achieved solid same-restaurant traffic growth, and our results were well ahead of those for the industry, which had a decline.

There is no question that there was considerable cost associated with the changes we made. Many of our promotional and core menu affordability efforts involved margin pressure and, in some cases, there was more pressure than we initially anticipated. In addition, as we reorganized Marketing and Operations, which involved putting tenured leaders in new places and adding new leaders, there was some adverse effect on execution that likely resulted in meaningful but difficult-to-measure cost. And, of course, there were the direct costs of the technology and other investments in additional capabilities that we made. However, we firmly believe that, given the criticality of arresting the same-restaurant traffic erosion we have been experiencing, these were costs worth incurring.

Looking Forward

As we look forward to fiscal 2014 and beyond, our top priority is to reestablish consistent same-restaurant traffic growth. And to achieve this goal we must respond more quickly and more effectively to the consumer and competitive dynamics that define our industry today.

As a result, we are tempering check average growth in fiscal 2014 because we think that is necessary to support traffic growth in the near term. As we do so, we are refining our affordability tactics based on what we learned during fiscal 2013 to moderate the margin pressure that often comes with lower check growth. In addition, we are significantly reducing new restaurant expansion at Olive Garden, going from the 35 to 40 net new openings we have had each year for the past few years to approximately 15. With this change, we believe the brand can better focus on regaining same-restaurant traffic momentum and on making the guest experience changes required for sustained success.

Finally, we are continuing to make other investments in future success. More specifically, we are investing in a select few initiatives to reshape the guest experiences we provide in ways that further respond to the dynamics that are the New Era. These include offering small plates at Olive Garden that can be enjoyed individually as a more affordable appetizer choice or combined to create a customized meal, introducing more up-to-date seafood options at Red Lobster like shrimp tacos and lobster tacos, and adding a new Chef’s Showcase section at LongHorn that highlights innovative and distinctive new items. In addition, we are investing to transition to the new healthcare landscape in a way that maintains strong employee engagement. And, we are continuing to invest in commercializing lobster aquaculture because such a breakthrough can help preserve Red Lobster’s ability to provide guests with price-accessible offerings for years to come.

Conclusion

As we make the changes required to operate successfully in a New Era, we have the needed resources. We have strong brands, considerable collective expertise and experience and a cost-effective operating support platform. Most important, we have a winning culture, with people who remain highly engaged despite a difficult fiscal 2013. A measure of the strength of our culture is our recognition by FORTUNE magazine in 2013 for the third consecutive year as one of the “100 Best Companies to Work For™.” We are particularly proud because selection relies on an independently administered survey of employees — which, in our case, are largely hourly restaurant employees — and Darden is the only restaurant company to receive such recognition.

Looking forward, the strong culture and wonderful people we have at Darden are the single biggest reasons why we are confident we will successfully make the changes required to better compete today and remain the industry leader tomorrow.

Thank you for being a stakeholder.

Clarence Otis, Jr.

Chairman and Chief Executive Officer

Andrew Madsen

President and Chief Operating Officer